Most homeowners who are eligible to remove PMI know they should look into it. Very few know exactly how the formal process works, what the lender actually requires, and where the process most commonly breaks down. This article walks through the specific steps, so you can move efficiently from eligibility to elimination.

Step One: Confirm Your Eligibility

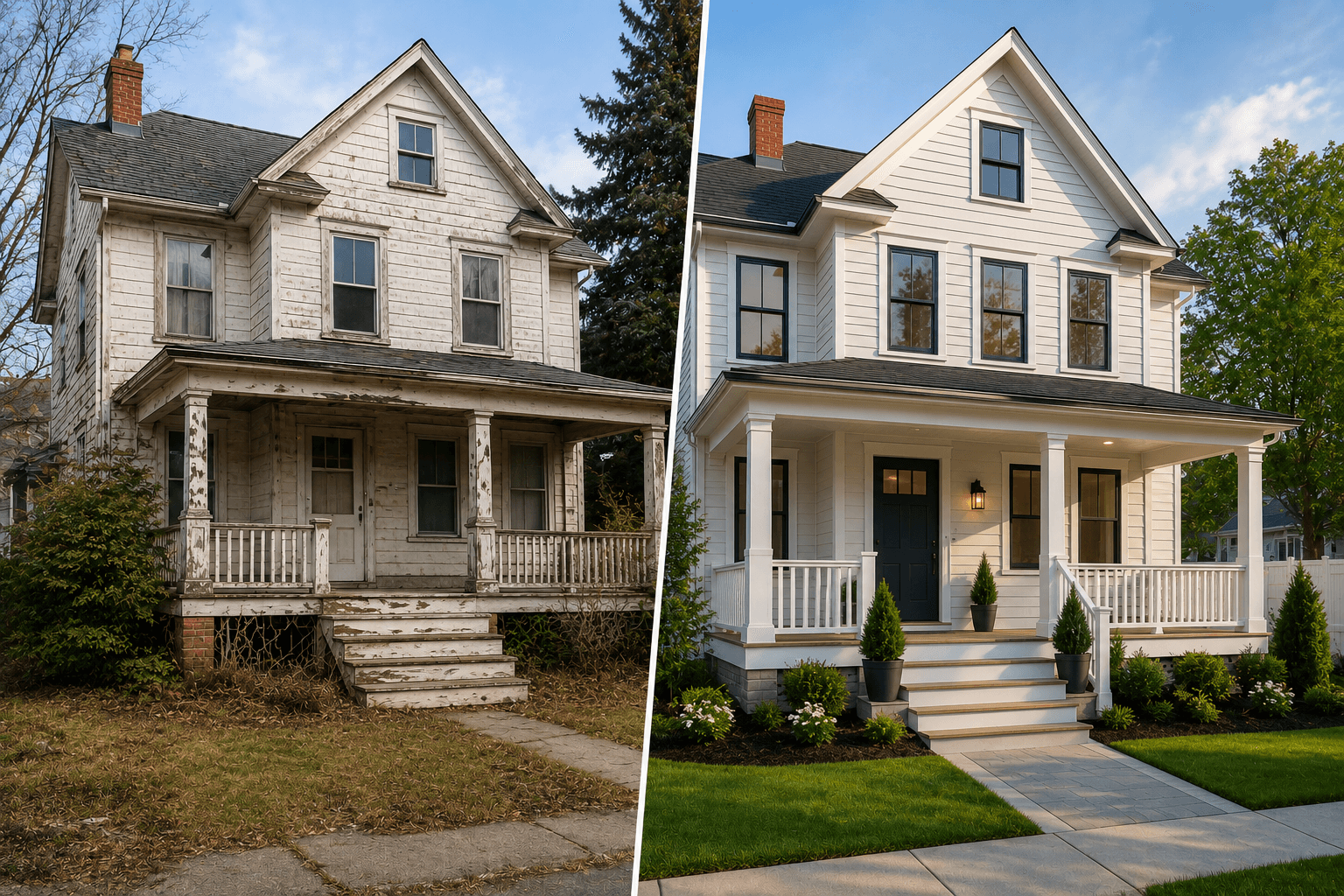

PMI cancellation eligibility is governed by the Homeowners Protection Act for conventional loans. There are two primary paths to eligibility. The first is scheduled amortization, when your outstanding balance reaches 78 percent of the original loan value through regular payments, the lender is legally required to cancel automatically. The second is current value, if your outstanding balance is at or below 80 percent of your home's current appraised market value, you can request cancellation.

For the appreciation-based path, the key number is your current loan balance divided by the appraised value you establish with a professional appraisal. Before contacting your lender, know your current outstanding balance from your mortgage statement.

Step Two: Understand Your Lender's Specific Requirements

Different lenders have different requirements for accepting a PMI cancellation request based on appreciation. Some require that you have owned the property for at least two years. Some require a minimum of 25 percent equity (75 percent LTV) rather than 20 percent if you have not held the loan for five years. And nearly all require a professional appraisal, but the specific requirements about who the appraiser is, what form the appraisal must take, and what fee they charge for review vary.

Contact your lender or servicer before commissioning any appraisal. Ask specifically: what are your requirements for a PMI cancellation request based on current appraised value? Get the requirements in writing if possible. Then commission the appraisal that meets those requirements.

Step Three: Commission the Appraisal

Once you have the lender's requirements, engage a certified residential appraiser with experience in the specific neighborhood and property type. The appraiser will physically inspect the property, research recent comparable sales, and produce a USPAP-compliant appraisal that your lender can rely on.

A May appraisal benefits from the spring comparable sale environment. If your lender permits a homeowner-commissioned appraisal (as opposed to a lender-ordered appraisal), commissioning it in May gives you the strongest possible market evidence to establish your current value.

Step Four: Submit the Formal Written Request

Most lenders require a formal written cancellation request that references the specific loan number, includes the appraisal documentation, confirms that the property has not been subject to any liens that would affect the equity calculation, and in some cases includes a certification that you have made on-time payments for the required period.

Once the request is received and the appraisal is reviewed, the lender typically responds within 30 days. If the appraisal supports the 80 percent LTV threshold, PMI cancellation is effective from a specified date and your monthly payment decreases accordingly.

Ready to Get Started?

Whether you are a homeowner, estate attorney, realtor, or investor in Greater Boston, Adam Wiener and the Aladdin Appraisal team deliver USPAP-compliant appraisals you can rely on. Call today: (617) 517-3711 | info@aladdinappraisal.com | aladdinappraisal.com