Fix-and-flip lending in Greater Boston has specific documentation requirements that separate funded deals from unfunded ones. The central document in that underwriting process is the appraisal, specifically, an appraisal that produces both an as-is value (the property today) and an after-repair value, or ARV (the property upon completion of planned improvements). Understanding how these two values are produced, and what makes them credible, is essential for investors seeking private financing.

What As-Is Value Actually Represents

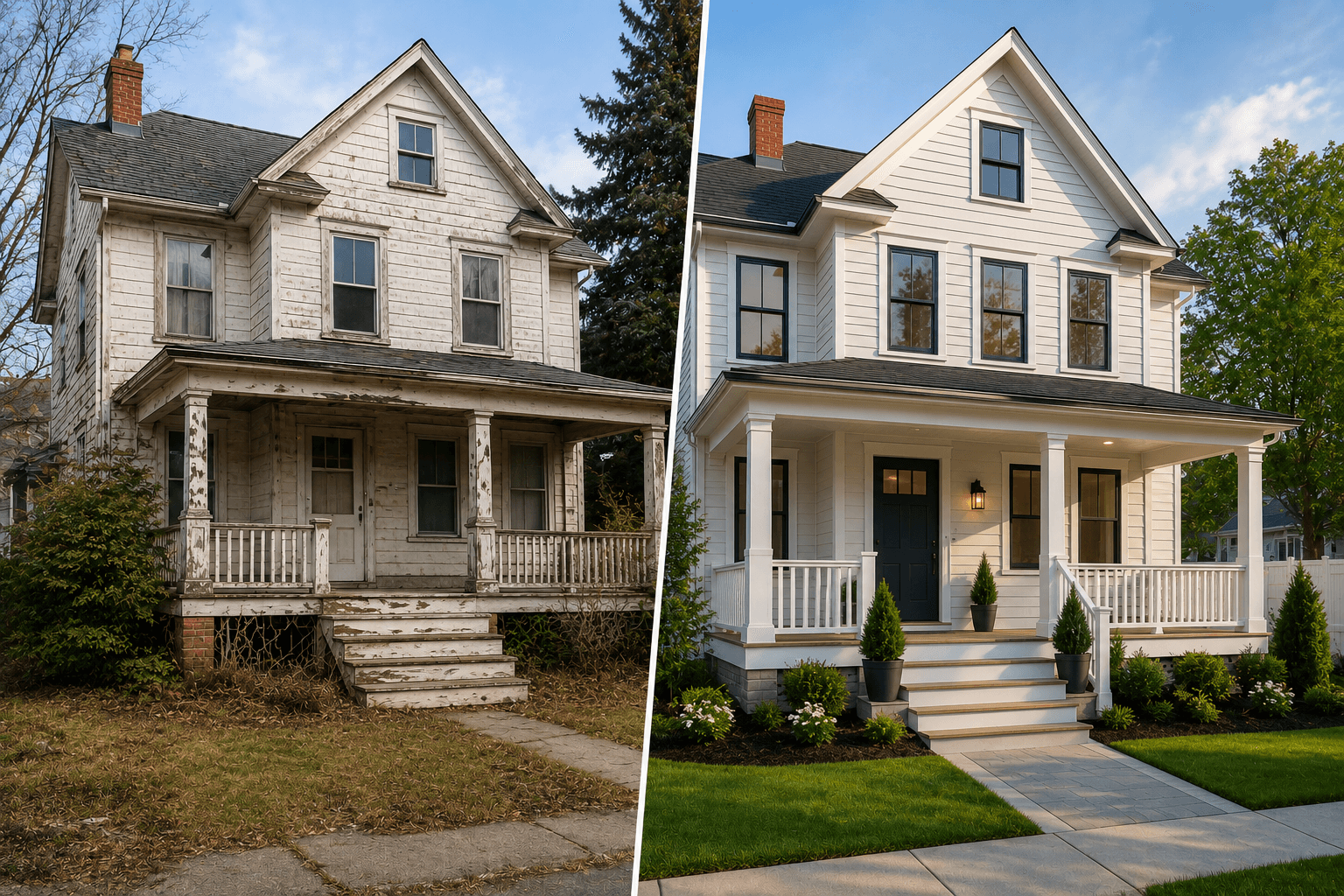

The as-is value is the professional opinion of what the property is worth in its current condition, on the open market, as of the date of inspection. For a property being acquired for renovation, the as-is value is typically below the eventual ARV, sometimes significantly. It reflects deferred maintenance, functional obsolescence, or dated condition that the renovation is intended to address.

The as-is value is important for the lender's risk calculation: if the borrower defaults before any renovation is completed, what can the lender recover? A property with a $450,000 as-is value and a $750,000 ARV represents a very different collateral risk than one with a $650,000 as-is value and a $750,000 ARV.

What Makes an ARV Opinion Credible

The ARV opinion is forward-looking. The appraiser must analyze the planned renovation scope, typically from a summary of planned work provided by the borrower, and establish what the property would sell for after that work is completed, in its intended improved condition.

A credible ARV opinion is built on renovated comparable sales: properties in the subject's market area that have been similarly renovated and sold, demonstrating what buyers actually pay for properties in the improved condition the subject will achieve. The appraiser analyzes the quality of the planned renovation, the relevance of the comparable sales to the subject's characteristics, and the current market absorption for properties at the projected ARV price point.

Why the Appraiser's Experience Matters for ARV

An ARV appraisal requires more professional judgment than a standard purchase appraisal. The appraiser is estimating a future condition, not documenting a current one. The comparable selection must account for renovation quality, not just the existence of renovation. And the appraiser must apply judgment about whether the planned scope is realistic, whether the comparable sales reflect the same quality level the subject will achieve, and whether the projected ARV is supportable at the intended price point.

Investors who submit ARV appraisals from appraisers without fix-and-flip or investment property experience often receive reports that lenders reject, not because the value is unsupportable, but because the methodology is not defensible. An experienced investment property appraiser knows what private lenders require and produces a report that meets that standard.

Ready to Get Started?

Whether you are a homeowner, estate attorney, realtor, or investor in Greater Boston, Adam Wiener and the Aladdin Appraisal team deliver USPAP-compliant appraisals you can rely on. Call today: (617) 517-3711 | info@aladdinappraisal.com | aladdinappraisal.com